Choosing the mortgage with the lowest monthly payment can cost you tens of thousands over 30 years.

This guide cuts through the noise and explains the five main loan types: fixed-rate, adjustable-rate (ARM), FHA, VA, and jumbo.

You’ll get clear rules to match a loan to how long you’ll stay, how steady your income is, how much you can put down, and whether you can handle payment swings.

Read on and you’ll know which mortgage type is likely the right fit for your financial situation.

Key Mortgage Types and When Each Is Best

A mortgage is one of the biggest financial commitments you’ll make. Most stretch 15 to 30 years. The type you pick shapes your monthly payment, what you’ll pay in interest, and how much risk you’re taking on. Five categories dominate the U.S. market: fixed-rate mortgages, adjustable-rate mortgages (ARMs), FHA loans, VA loans, and jumbo loans. Each one targets different credit situations, down payment amounts, and how long you plan to stay.

Fixed-rate mortgages lock your interest rate for the full term. Your monthly principal and interest stay the same from day one to the last payment. ARMs start with a lower rate for a set window (usually three, five, or seven years), then adjust based on market benchmarks. FHA loans are government-backed and allow down payments as low as 3.5 percent. They’ll accept credit scores below what conventional lenders want. VA loans, backed by the Department of Veterans Affairs, don’t require a down payment or mortgage insurance if you’re an eligible service member or veteran. Jumbo loans are for purchases above the conforming loan limit (set each year by the Federal Housing Finance Agency). They need stronger credit and bigger down payments.

Your right match depends on four things: how long you’ll stay in the home, how stable your income is, what you can put down, and whether payment changes are something you can handle. Planning to stay more than seven years and want predictability? Fixed-rate is usually safest. Expecting to sell or refinance within five years and want the lowest starting rate? An ARM could save you thousands. Credit score below 620 or less than 10 percent saved? FHA or VA loans often offer better access. Buying above the conforming limit? You’ll need a jumbo and the stronger financial profile that goes with it.

Here’s a quick match guide:

Fixed-rate mortgage: Best if you’re staying long term or want stable payments and think rates will rise.

Adjustable-rate mortgage (ARM): Best if you’re selling or refinancing within three to seven years, or you’re confident rates will stay flat or drop.

FHA loan: Best for first-time buyers, credit scores between 580 and 620, or down payments under 10 percent.

VA loan: Best for eligible veterans, active-duty members, and qualifying spouses who want to skip the down payment and mortgage insurance.

Jumbo loan: Best for buying above the conforming limit with strong credit (usually above 700) and at least 10 to 20 percent down.

How Fixed-Rate Mortgages Work

A fixed-rate mortgage keeps the same interest rate from closing day until payoff. That means your monthly principal and interest stay constant for 180 months on a 15-year loan or 360 months on a 30-year. The rate you lock at closing is what you pay the whole way. Rates climb? Your payment doesn’t budge. Rates drop? Still no change unless you refinance.

Under the surface, fixed-rate mortgages use an amortization schedule that splits each payment into principal (what you borrowed) and interest (borrowing cost). Early on, most goes to interest. Over time, more chips away at principal. By the final year, almost everything is principal. Longer terms mean more total interest but lower monthly payments. A 30-year fixed at 4.00 percent on $200,000 runs about $955 monthly and roughly $143,740 in total interest. Same loan on a 15-year term at 3.00 percent bumps the payment to about $1,381 but slashes total interest to around $48,610. You pay $426 more each month but save about $95,130 over the life of the loan.

Fixed-rate mortgages are the most common type in the U.S. Lenders offer them in conventional (not government-backed) and government-backed versions, including FHA and VA fixed-rate products. The stability appeals to anyone planning to stay for years or who wants to budget without worrying about rate resets. If you value predictability over minimizing that initial payment, fixed-rate is usually where you start.

Who Fixed-Rate Mortgages Are Best For

Fixed-rate mortgages fit borrowers who want payment stability and expect to own the home seven years or longer. Staying through retirement? Raising kids in the property? Just want the certainty that your housing cost won’t shift? A fixed-rate loan removes interest-rate risk from your budget. That stability gets even more valuable when rates are low at purchase. Lock in 3.00 or 4.00 percent and you’re protected if rates jump to 6.00 or 7.00 percent down the road.

Fixed-rate products also work for borrowers with steady income who can handle slightly higher initial payments in return for long-term savings. A 15-year fixed requires a bigger monthly payment than a 30-year, but it typically carries a lower rate and cuts total interest by tens of thousands. If your income is reliable and you’ve got budget room, the 15-year structure accelerates equity and reduces borrowing cost.

Consider fixed-rate if you:

Plan to stay in the home more than seven to 10 years

Want predictable monthly housing costs that won’t shift

Expect rates to rise or stay flat

Have stable income and prefer paying less total interest even if it means a higher payment now

Requirements for Fixed-Rate Mortgages

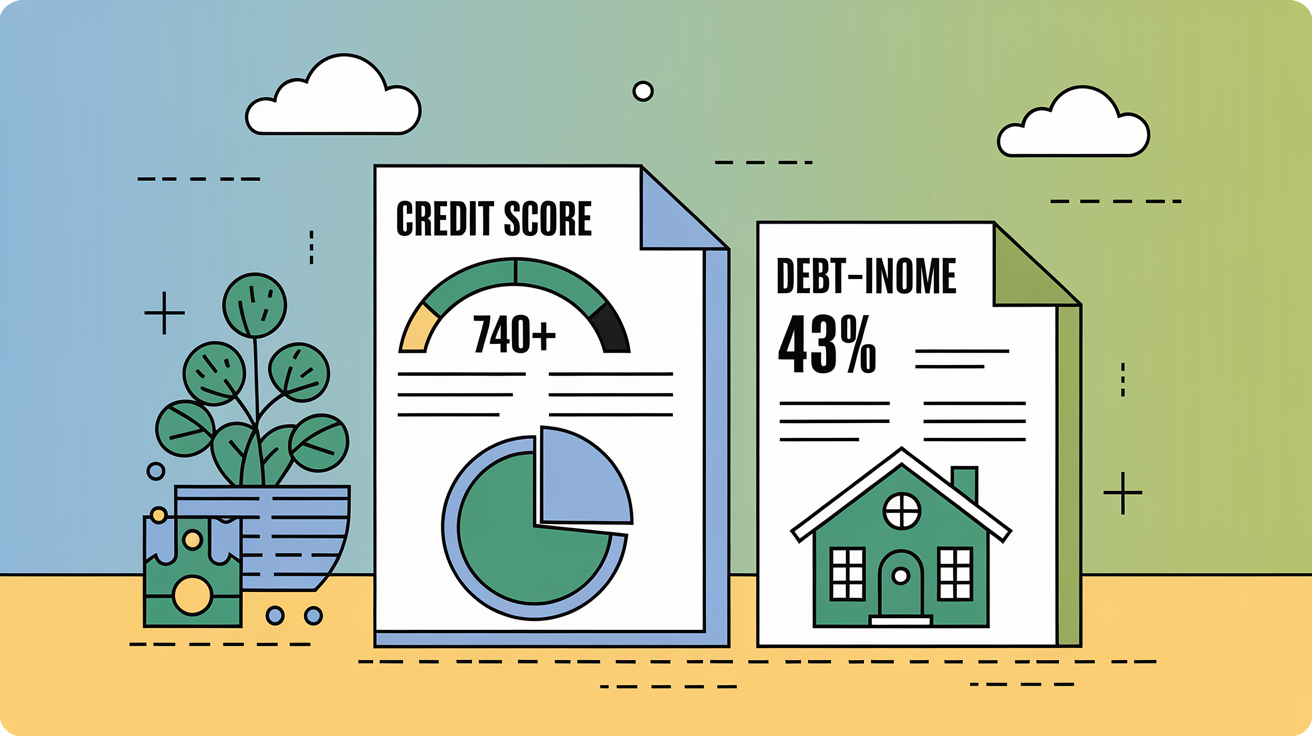

Lenders evaluate fixed-rate applications using three core factors: credit score, debt-to-income ratio (DTI), and down payment. For conventional fixed-rate loans, most want a credit score above 620. Scores above 740 typically unlock the lowest rates. Score between 620 and 680? You can still qualify, but expect a higher rate. Below 620, conventional lenders often decline or require things like a larger down payment or lower DTI.

Debt-to-income measures your total monthly debt payments (mortgage, car loans, credit cards, student loans) divided by gross monthly income. Most lenders want DTI below 43 percent for qualified mortgages, though some allow up to 50 percent if you have strong credit and reserves. Housing costs alone (principal, interest, property taxes, insurance, HOA) should stay below 30 percent of gross income. Down payment varies: putting down at least 20 percent eliminates private mortgage insurance (PMI) on conventional loans. Less than 20 percent? You’ll pay PMI until your balance drops below 80 percent of the home’s value. Government-backed fixed-rate loans (FHA, VA) have their own down payment and insurance rules but follow similar DTI guidelines.

Key qualification factors:

Credit score 620 or higher (740+ for best rates on conventional)

Debt-to-income below 43 percent (housing costs below 30 percent preferred)

Down payment at least 3 to 5 percent (20 percent to skip PMI on conventional)

How Adjustable-Rate Mortgages Work

An adjustable-rate mortgage starts with an initial fixed period, then adjusts at regular intervals based on a market index. Common ARM structures are 3/1, 5/1, and 7/1. First number is the fixed period (in years), second is how often it adjusts after that (once per year). A 5/1 ARM holds your rate steady for 60 months, then resets annually for the remaining term. During the fixed period, the ARM typically offers a lower rate than a comparable 30-year fixed. That lower rate translates to a smaller monthly payment and less interest paid early on.

After the initial period ends, the lender recalculates your rate by adding a margin (a fixed percentage in your loan docs) to a benchmark index (commonly the Secured Overnight Financing Rate, or SOFR). If the index has risen, your rate and payment go up. If it’s fallen, they go down. Most ARMs include rate caps that limit how much your rate can shift in a single adjustment and over the loan’s life. A typical cap structure might be 2/2/5: your rate can rise no more than 2 percent at the first adjustment, 2 percent at each following adjustment, and 5 percent total over the loan’s life. Without caps, an ARM could become unaffordable if rates spike.

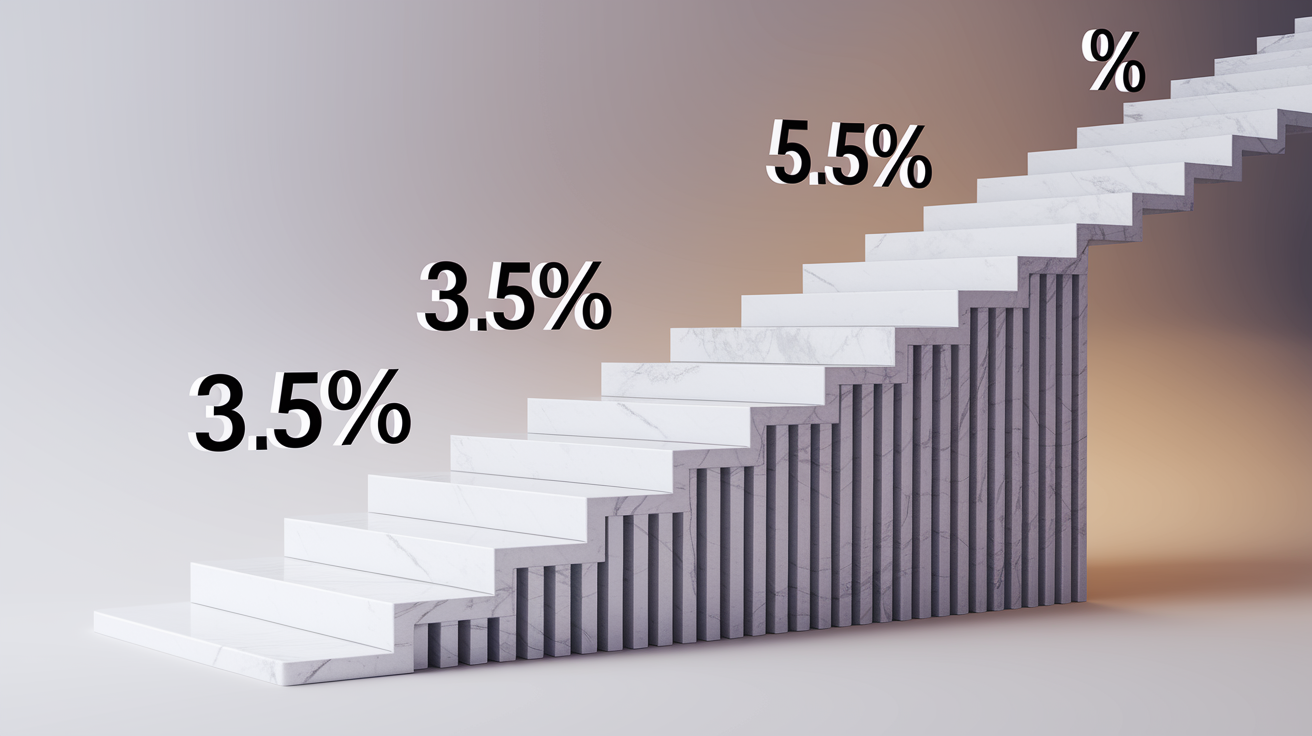

The appeal is front-loaded savings. Borrow $300,000 and a 5/1 ARM offers 3.50 percent while a 30-year fixed is 4.25 percent? You’ll save roughly $125 monthly during the first five years, about $7,500 total. The risk is year six. If you haven’t sold or refinanced by then, your rate could jump to 5.50 percent or higher, erasing those early savings. ARMs work best when you’re certain you’ll exit before the adjustment period starts.

Who Adjustable-Rate Mortgages Are Best For

ARMs suit borrowers who plan to sell or refinance within the initial fixed window. Buying a starter home and expect to move in four years? A 5/1 ARM lets you capture a lower rate without exposure to future adjustments. Anticipating a major income jump (finishing a residency, earning partnership) and planning to refinance to a shorter fixed term? An ARM keeps your payment low meanwhile. The product also appeals in markets where home prices are climbing fast and you expect to build equity quickly enough to refinance or sell before the first reset.

ARMs can also work if you think rates will stay flat or drop. Lock in an ARM at 3.50 percent and rates fall to 3.00 percent by the time your loan adjusts? Your new rate might be lower than your starting rate. That’s less common, but possible in a falling-rate environment. The key is honest assessment of your timeline and risk tolerance. Any chance you’ll stay past the fixed period and rates could rise? The ARM’s initial savings may not justify the uncertainty.

Consider an adjustable-rate mortgage if you:

Plan to sell or refinance within three to seven years (before the first adjustment)

Want the lowest possible monthly payment during the initial fixed period

Expect significant income growth that lets you refinance or pay off the loan early

Think rates will stay stable or decline over the next several years

Requirements for Adjustable-Rate Mortgages

Lenders underwrite ARMs using the same credit score, DTI, and down payment criteria as fixed-rate loans, but they often add an extra step: qualifying you at a higher rate. Some require your DTI to stay below 43 percent even if the rate adjusts to the maximum allowed under the cap structure. This ensures you can afford the payment if rates spike. For example, applying for a 5/1 ARM with a starting rate of 3.50 percent and a lifetime cap of 8.50 percent? The lender may calculate your DTI as if the rate were already 8.50 percent. Pass that test and you’re approved. Fail and the lender may reduce your loan amount or require a bigger down payment.

Credit score requirements for ARMs typically mirror fixed-rate products: 620 minimum for conventional ARMs, higher scores for the best rates. Down payment expectations also match fixed-rate loans, with 20 percent down eliminating PMI on conventional ARMs. Because ARMs carry rate risk, some lenders prefer borrowers with strong credit and stable income. Marginal score or variable income? A fixed-rate product may be easier to qualify for and safer long term.

Key qualification considerations for ARMs:

Credit score 620 or higher (740+ for best introductory rates)

Debt-to-income below 43 percent, sometimes calculated at the fully indexed rate

Down payment at least 3 to 5 percent (20 percent to skip PMI); lenders may require higher down payments if your credit is below 700

Understanding FHA Loans

FHA loans are mortgages insured by the Federal Housing Administration, a government agency inside the U.S. Department of Housing and Urban Development. The FHA doesn’t lend directly. It guarantees loans made by approved private lenders. That guarantee cuts the lender’s risk, letting them approve borrowers with lower credit scores and smaller down payments than conventional loans typically allow. Minimum down payment for an FHA loan is 3.5 percent if your credit score is 580 or higher. Score between 500 and 579? You’ll need at least 10 percent down. Below 500 generally doesn’t qualify.

FHA loans require two types of mortgage insurance. The upfront mortgage insurance premium (UFMIP) is 1.75 percent of the loan amount, usually rolled into the loan balance at closing. The annual mortgage insurance premium (MIP) ranges from 0.45 to 1.05 percent of the loan balance, divided into 12 monthly payments. Put down less than 10 percent and MIP stays for the life of the loan. Put down 10 percent or more and MIP drops off after 11 years. Unlike private mortgage insurance on conventional loans, FHA MIP can’t be removed by reaching 20 percent equity. You must refinance into a conventional loan to eliminate it.

FHA loans come in both fixed-rate and adjustable-rate versions, with 15 or 30 year terms. They’re commonly used by first-time buyers who’ve saved enough for a small down payment but lack the credit history or score for a conventional loan. FHA loans also allow higher DTI ratios (up to 50 percent in some cases) and permit gifts or grants to cover the down payment and closing costs, making homeownership more accessible for buyers with limited savings.

Who FHA Loans Are Best For

FHA loans are designed for borrowers with lower credit scores, smaller down payments, or higher debt-to-income ratios. Credit score between 580 and 620? An FHA loan may be your only option without a co-signer or much larger down payment. Saved 3.5 percent for a down payment but can’t reach the 5 or 10 percent conventional lenders prefer? The FHA product opens the door. First-time buyers often choose FHA because the flexible requirements match their financial profile: steady income, some savings, but not enough credit history or cash reserves to meet conventional standards.

FHA loans also work for buyers who’ve had financial setbacks like bankruptcy or foreclosure. The FHA lets you qualify two years after a Chapter 7 bankruptcy discharge or three years after a foreclosure, compared to four to seven years for most conventional loans. Rebuilding credit and need to buy sooner? The FHA timeline can make a real difference.

Consider an FHA loan if you:

Have a credit score between 580 and 620 and struggle to qualify for conventional

Can afford a 3.5 percent down payment but not the 10 to 20 percent conventional lenders prefer

Are a first-time buyer with limited credit history or savings

Have recovered from bankruptcy or foreclosure and need to buy within two to three years

Requirements for FHA Loans

FHA loan requirements are more flexible than conventional standards but still include credit, income, and property criteria. Minimum credit score is 580 for a 3.5 percent down payment and 500 for a 10 percent down payment, though many FHA lenders set their own overlays and require scores above 600. Your debt-to-income can go as high as 50 percent if you have compensating factors like significant cash reserves or a strong payment history, but most lenders prefer DTI below 43 percent. The property must meet FHA minimum property standards, meaning it’s safe, sound, and secure. Homes with significant defects or health hazards (peeling lead paint, failing roof) won’t pass the FHA appraisal until repairs are done.

FHA loans also require the home be your primary residence. You can’t use an FHA loan for an investment property or second home. Mortgage insurance premiums are mandatory, adding to your monthly cost. On a $200,000 FHA loan with 3.5 percent down, the upfront premium is $3,500 (usually financed) and the annual premium is roughly $1,680 per year, or $140 monthly, if your down payment is below 10 percent. That insurance cost stays until you refinance or pay off the loan.

Key FHA qualification criteria:

Minimum credit score 580 for 3.5 percent down (500 for 10 percent down), though lender overlays often require 600 or higher

Debt-to-income below 43 to 50 percent depending on compensating factors

Property must meet FHA minimum property standards and serve as your primary residence; upfront and annual mortgage insurance premiums required

Understanding VA Loans

VA loans are mortgages guaranteed by the U.S. Department of Veterans Affairs for eligible veterans, active-duty service members, certain National Guard and Reserve members, and surviving spouses. The VA guarantee lets lenders offer terms unmatched by any other mortgage product: no down payment required, no private mortgage insurance, competitive interest rates, and flexible credit requirements. The VA doesn’t set a minimum credit score, but most lenders require at least 580 to 620. The VA does charge a one-time funding fee ranging from 1.4 to 3.6 percent of the loan amount, depending on your down payment (if any), whether you’ve used your VA benefit before, and your service category. Veterans with service-connected disabilities are exempt from the funding fee.

VA loans can be used to purchase a primary residence, build a home, or refinance an existing mortgage. The property must meet VA minimum property requirements, similar to FHA standards but with additional safety and livability criteria. VA loans also let you finance up to 100 percent of the home’s value with no monthly mortgage insurance, a benefit that can save hundreds monthly compared to FHA or conventional loans with low down payments. The absence of PMI or MIP makes VA loans one of the most cost-effective products available, especially for buyers who’d otherwise put down less than 20 percent.

VA loans come in fixed-rate and adjustable-rate versions, with 15 and 30 year terms available. The VA sets limits on certain closing costs lenders and sellers can charge, which can reduce your upfront expenses. Because the government guarantees part of the loan, lenders face less risk and are often willing to approve borrowers with lower credit scores or higher DTI ratios than conventional guidelines allow.

Eligibility Criteria for VA Loans

VA loan eligibility depends on your length and type of military service. Active-duty service members generally become eligible after 90 consecutive days during wartime or 181 days during peacetime. Veterans must have served the minimum required period and received a discharge that’s anything other than dishonorable. National Guard and Reserve members typically need six years of service to qualify. Surviving spouses of service members who died in the line of duty or from service-connected disabilities may also be eligible if they haven’t remarried (or remarried after age 57).

To apply for a VA loan, you must get a Certificate of Eligibility (COE) from the VA, which confirms your service history and entitlement. Lenders use the COE to verify you qualify for the VA guarantee. You can request a COE online through the VA’s eBenefits portal, through your lender, or by mail. The process is usually quick, often done within a few days. Once you have the COE, the lender will evaluate your credit, income, and DTI just as they would for any other mortgage, but the VA’s backing gives you access to better terms and more flexibility than most civilian borrowers get.

VA loan eligibility checklist:

Active-duty service members with 90 days (wartime) or 181 days (peacetime) of consecutive service

Veterans who served the minimum required period and received a discharge other than dishonorable

National Guard and Reserve members with at least six years of service

Surviving spouses of service members who died on active duty or from service-connected disabilities (if not remarried, or remarried after age 57)

Understanding Jumbo Loans

Jumbo loans are mortgages that exceed the conforming loan limit set annually by the Federal Housing Finance Agency. For 2024, the conforming limit is $766,550 in most U.S. counties and higher in expensive markets like San Francisco, New York, and parts of Southern California. Any loan above that threshold is considered non-conforming and can’t be purchased by Fannie Mae or Freddie Mac, the two government-sponsored enterprises that buy and securitize most conventional mortgages. Without that secondary-market support, lenders take on more risk, so they impose stricter underwriting standards and often charge slightly higher interest rates.

Jumbo loans are typically used to purchase high-value properties in competitive markets. Because the loan amounts are large (often $1 million or more), lenders want assurance you can handle the payment even if your income drops or the housing market softens. That means jumbo underwriting focuses heavily on credit score, cash reserves, debt-to-income ratio, and down payment. Many jumbo lenders require credit scores above 700, down payments of 10 to 20 percent, and DTI ratios below 43 percent. Some also require proof of liquid reserves equal to six to 12 months of mortgage payments.

Jumbo loans come in both fixed-rate and adjustable-rate versions, with 15 and 30 year terms available. Rates on jumbo loans used to be significantly higher than conforming rates, but that gap has narrowed in recent years. In some cases, well-qualified borrowers can secure jumbo rates that match or even beat conforming rates, especially if they put down 20 percent or more. The key is meeting the lender’s risk criteria: strong credit, low leverage, and documented ability to repay.

Requirements for Jumbo Loans

Jumbo loan underwriting is stricter than conventional or government-backed products because lenders hold the full risk on their balance sheets or sell them to private investors with tighter standards. Most jumbo lenders require a credit score of at least 700, with many preferring 740 or higher to qualify for the best rates. Your debt-to-income should stay below 43 percent, and some lenders cap it at 38 percent for jumbo products. Down payment requirements typically range from 10 to 20 percent, though some lenders will go as low as 5 percent if you have exceptional credit and significant reserves.

Cash reserves are a major factor in jumbo underwriting. Lenders want to see you have liquid assets (savings, investments, retirement accounts) equal to six to 12 months of mortgage payments after closing. This reserve requirement protects the lender if you lose your job or face a financial emergency. Documentation requirements are also more rigorous: expect to provide two years of tax returns, recent pay stubs, bank statements, and proof of assets. Self-employed borrowers will need to show consistent income over at least two years, often verified through tax returns and profit-and-loss statements.

Key jumbo loan requirements:

Credit score 700 or higher (740+ for best rates and terms)

Down payment 10 to 20 percent (some lenders allow 5 percent with strong credit and reserves)

Liquid reserves equal to six to 12 months of mortgage payments after closing; full income documentation and debt-to-income below 43 percent

Practical Framework for Choosing the Right Mortgage

Choosing the right mortgage starts with four questions: How long will you stay in the home? How stable is your income? How much can you put down? What’s your credit score? Your answers filter the five major product types (fixed-rate, ARM, FHA, VA, jumbo) down to the one or two that match your financial situation. Planning to stay more than 10 years, expect steady income, have a credit score above 680 with 10 to 20 percent down? A conventional fixed-rate mortgage is usually the safest and most cost-effective choice. Planning to sell or refinance within five years and want the lowest initial payment? A 5/1 ARM may save you thousands in interest during the early years.

Credit score between 580 and 620 or less than 5 percent saved? An FHA loan opens the door with flexible requirements and a low down payment, though you’ll pay mortgage insurance for the life of the loan unless you refinance. Eligible veteran or active-duty service member? A VA loan offers unbeatable terms: no down payment, no mortgage insurance, competitive rates. Buying above the conforming loan limit with strong credit? A jumbo loan is your only option, requiring a larger down payment and stricter underwriting but delivering the financing you need for a high-value property.

Use this six-step decision framework to pick your mortgage:

Calculate your affordable monthly payment. Take your gross monthly income, multiply by 0.30, and use that as your housing-cost ceiling (principal, interest, taxes, insurance, HOA). Subtract property taxes, insurance, and HOA to find your maximum principal-and-interest budget.

Check your credit score. Above 740 unlocks the best rates on conventional and jumbo loans. Between 620 and 740, you’ll qualify but pay higher rates. Between 580 and 620, FHA is often your best option. Below 580, work on credit repair before applying.

Set your down payment target. Can you put down 20 percent? You’ll avoid PMI on conventional loans and unlock better jumbo terms. Have 10 percent? Conventional is still possible. Have 3.5 to 5 percent? FHA is accessible. Veteran with 0 percent down? VA is the clear winner.

Estimate your ownership timeline. Staying more than seven years favors fixed-rate mortgages. Selling or refinancing within three to five years favors ARMs. Short timelines also make FHA viable even with lifetime MIP, since you’ll exit before paying much insurance.

Compare total cost, not just monthly payment. Use a mortgage calculator to model principal, interest, insurance, and total interest paid over the loan term. A 15-year loan saves tens of thousands in interest but raises your monthly payment. A 30-year loan lowers the payment but costs more over time. An ARM saves money early but risks higher payments later.

Shop at least three lenders. Get written offers from a bank, a credit union, and an online lender. Compare APR (which includes interest rate plus fees), origination charges, discount points, and total closing costs. The lowest rate isn’t always the best deal if fees are high.

Final Words

in the action, we laid out the main mortgage types—fixed-rate, adjustable-rate, FHA, VA, and jumbo—and when each one fits. You saw how fixed and ARM payments work, typical requirements, and who benefits most.

Use the step-by-step framework: match your timeline, check credit and down payment, and weigh the trade-offs. This clear guide to choosing the right mortgage type gives you a simple path forward. With the right facts, you’ll pick a loan that fits your plans.

FAQ

Q: What are the main mortgage types and how do they differ?

A: The main mortgage types are fixed-rate, adjustable-rate (ARM), FHA, VA, and jumbo loans. They differ by rate stability, eligibility rules, down payment needs, insurance, and loan size.

Q: What is a fixed-rate mortgage and how does it work?

A: A fixed-rate mortgage is a loan that keeps the same interest rate for the term, usually 15 or 30 years, giving predictable monthly principal and interest payments and steady amortization.

Q: Who is a fixed-rate mortgage best for?

A: A fixed-rate mortgage is best for buyers planning to stay long-term or who want payment certainty, especially if you expect rates to rise or prefer straightforward budgeting.

Q: What is an adjustable-rate mortgage (ARM) and how does it work?

A: An ARM is a loan with a lower initial fixed rate that then adjusts periodically based on a market index, subject to caps, offering cheaper short-term payments but future rate risk.

Q: Who should consider an ARM?

A: An ARM is for buyers who plan to sell or refinance before adjustments, or who accept rate risk in exchange for lower initial payments and short-term savings.

Q: What is an FHA loan and who is it best for?

A: An FHA loan is a government-backed mortgage allowing down payments as low as 3.5% and looser credit rules, best for first-time buyers or people with limited savings.

Q: What are the typical FHA loan requirements?

A: Typical FHA loan requirements include a minimum 580 credit score for 3.5% down, mandatory mortgage insurance premiums, and lender checks on income and property standards.

Q: What is a VA loan and who qualifies?

A: A VA loan is a benefit for eligible veterans, active-duty members, and some spouses; it often requires no down payment or mortgage insurance and needs a Certificate of Eligibility.

Q: What is a jumbo loan and when do you need one?

A: A jumbo loan finances amounts above conforming loan limits. You need one when the home price exceeds those limits and you can meet stricter credit and documentation rules.

Q: What are typical jumbo loan requirements?

A: Typical jumbo loan requirements include credit scores above 700, down payments of 10–20%, lower debt-to-income ratios, and thorough income and asset documentation.

Q: What do lenders look for when qualifying for a fixed-rate mortgage?

A: Lenders for fixed-rate mortgages focus on higher credit scores, a solid debt-to-income ratio, steady income, and larger down payments to secure the best rates.

Q: What unique qualification checks apply to ARMs?

A: ARM lenders often test your ability to afford payments at the fully indexed rate, plus they review credit, income, and debt-to-income similar to fixed-rate underwriting.

Q: How should I choose the right mortgage type?

A: To choose a mortgage, match your expected time in the home, risk tolerance, income stability, and down payment. Prioritize fixed rates for long stays, ARMs for short-term plans.

{kind=link}