Think APR and APY are the same?

They’re not—and that mix-up can cost you real money.

APR is the yearly rate lenders and card issuers advertise; APY shows what actually happens after interest compounds.

A 24 percent APR with daily compounding, for example, ends up roughly 27.1 percent effective—big difference on a $1,000 balance.

This post explains the math in plain terms, shows quick conversions, and tells you when to focus on APR or APY so you can avoid surprise fees and earn more on savings.

Core Differences Between APR and APY Explained Clearly

APR (Annual Percentage Rate) is what you’ll see plastered on loan offers and credit card mailers. It’s simple multiplication: take the periodic rate and multiply by the number of periods in a year. A credit card charging 2 percent monthly? That’s 2 percent × 12 = 24 percent APR. Loan APRs usually fold in fees like origination charges, which explains why the advertised number can run higher than the base interest rate. What APR doesn’t do is account for how often interest compounds during the year. It treats the cost as if interest gets calculated once annually or spreads evenly across periods.

APY (Annual Percentage Yield) tells you what actually happens when compounding enters the picture. The formula is APY = (1 + r/n)^n − 1, where r is the nominal rate and n is compounding frequency. Say you deposit cash at 6 percent APR with monthly compounding. Interest gets added to your balance twelve times a year, and each new chunk of interest starts earning its own interest the next month. That compounding effect pushes the real annual yield to 6.1678 percent APY. Slightly higher than the 6 percent APR. APY shows what you truly earn or pay after all the math plays out.

The gap between APR and APY comes down to compounding frequency. APR treats the year as one flat stretch. APY measures what happens when interest gets calculated and reinvested multiple times within that year. More frequent compounding? Bigger gap. At high rates or high compounding frequencies, that gap starts mattering in real dollars.

Compounding inclusion: APR ignores intra-year compounding. APY bakes it in and shows the real annual rate.

Fees: Loan APRs often bundle origination and certain financing fees. APY for deposits typically skips account fees.

Typical use: APR is standard for advertising loan costs and credit card rates. APY is the go-to for comparing savings accounts, CDs, and money market yields.

How APR and APY Are Calculated Using Real Formulas

APR is straightforward. Take the interest rate per period and multiply by the number of periods. If a lender charges 0.33333 percent monthly, that’s 0.33333 × 12 = 4 percent APR. When fees get involved, lenders annualize the total finance charge (interest plus certain upfront costs) over the loan term and express it as a percentage of principal. Either way, APR doesn’t raise anything to a power or multiply interest on interest.

APY uses exponential compounding. The formula: APY = (1 + r/n)^n − 1. Start with the nominal annual rate r, divide by compounding periods n, add 1, raise that sum to the power n, subtract 1. For a 6 percent nominal rate compounded monthly, that’s (1 + 0.06/12)^12 − 1 ≈ 0.061678 or 6.1678 percent APY. Same 6 percent compounding daily (n = 365)? APY climbs to roughly 6.1836 percent. The table below breaks down the three main rate expressions.

| Rate Type | Formula | What It Shows |

|---|---|---|

| APR (nominal) | periodic rate × n | Annualized rate without compounding, sometimes including fees |

| APY (monthly compounding) | (1 + r/12)^12 − 1 | Effective annual yield with interest compounded twelve times per year |

| APY (daily compounding) | (1 + r/365)^365 − 1 | Effective annual yield with daily reinvestment of interest |

When you see an offer listing 6.00 percent APR with monthly compounding, plug the numbers into the APY formula and you’ll get the true annual return of 6.1678 percent. Daily compounding? Use n = 365 and land at 6.1836 percent APY. The formulas are exact, the inputs are disclosed, and the math explains why two accounts with identical nominal APRs can deliver different actual returns.

Practical Differences Between APR and APY in Real Usage

APR is a nominal rate. It tells you the annualized percentage before any within-year compounding kicks in. Banks use APR to advertise loan costs because it simplifies comparison shopping and satisfies regulatory disclosure rules. Because APR often includes certain fees, it can run higher than the simple periodic interest rate you pay each month. A mortgage with a 4.00 percent nominal interest rate might carry a 4.15 percent APR after origination points get factored in.

APY is an effective rate. It answers “What’s my actual annual return or cost after all compounding is finished?” When a savings account compounds interest monthly, each month’s interest payment becomes part of the principal for the next month. That compounding loop increases the effective yield above the nominal rate. For continuously compounded accounts (rare in consumer finance but common in some investment models), the formula becomes APY = e^(APR_continuous) − 1, where e is Euler’s number, roughly 2.71828. Continuous compounding represents the mathematical limit as compounding frequency approaches infinity.

In practice, APR is the metric for loans, mortgages, auto financing, and credit cards because it includes fees and offers a standardized cost figure. APY is standard for deposit accounts, certificates of deposit, money market funds, and bond yields because it captures the true earning power of an investment. If you compare an APR loan rate to an APY savings rate without converting one to match the other, you’re comparing a nominal figure to an effective figure and your decision will be distorted.

Why APR vs APY Differences Matter for Borrowers and Savers

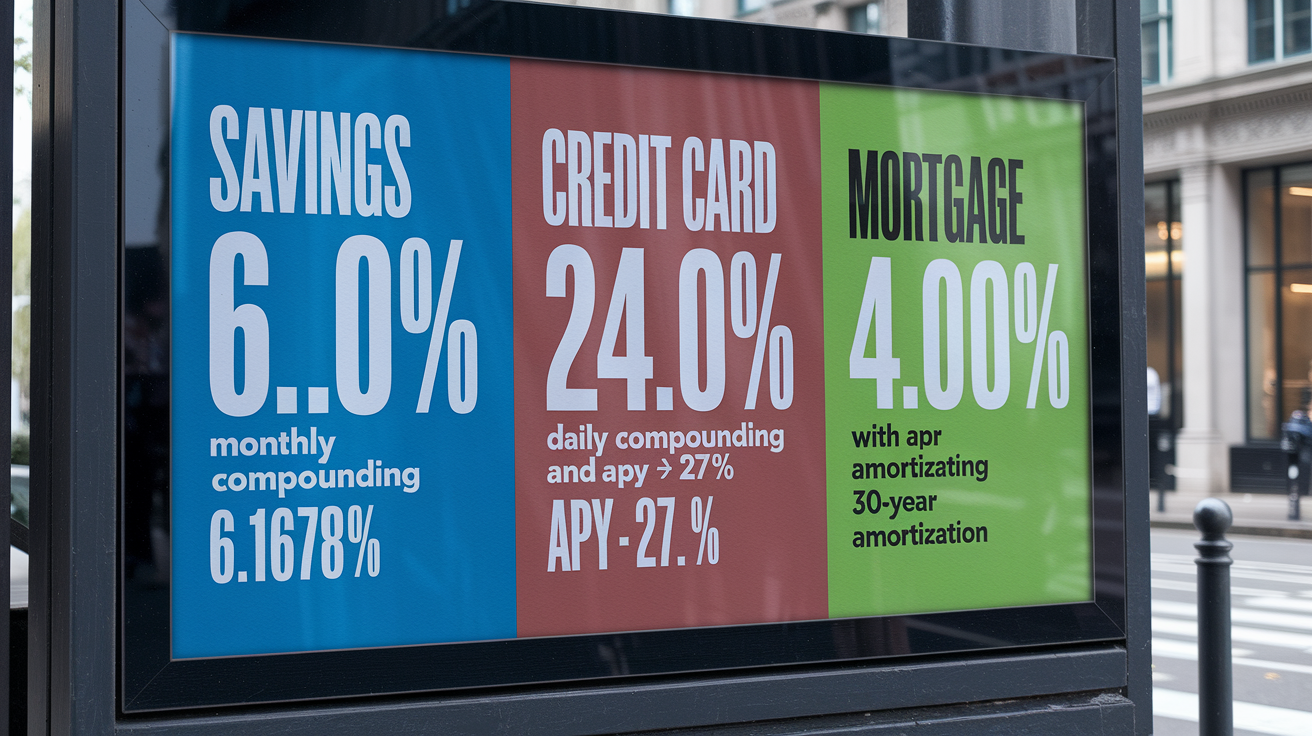

When you borrow, higher compounding frequency increases your true cost. A credit card advertising 24.00 percent APR usually compounds interest daily. Plug that into the APY formula: (1 + 0.24/365)^365 − 1 ≈ 0.271 or roughly 27.1 percent effective annual rate. Carry a $1,000 balance for a full year without any payments and you’ll owe around $1,271.25, not $1,240. That extra $31.25 comes purely from daily compounding. The higher the APR, the more painful daily compounding becomes.

When you save, compounding works in your favor. A savings account offering 6.00 percent APR with monthly compounding delivers an APY of 6.1678 percent. Deposit $1,000 and after one year you’ll have $1,061.68, not $1,060. The difference is only $1.68 on a thousand dollars, but scale that to $100,000 and the compounding bonus becomes $168 per year. Small APY differences stack up over time and across large balances. A 0.1 percent APY edge is worth $100 annually per $100,000 principal.

Mortgages show the long tail of APR. A $300,000 loan at 4.00 percent APR (nominal, monthly compounding) produces a monthly payment around $1,432. The monthly interest rate is 0.04 ÷ 12 ≈ 0.003333. Over 360 months, total payments hit roughly $515,520, meaning you pay about $215,520 in interest. If the lender charged a 1-point origination fee ($3,000), the disclosed APR might be closer to 4.15 percent, even though your monthly payment still gets driven by the 4.00 percent nominal rate. APR helps you compare the all-in cost across lenders with different fee structures.

Credit cards: A 24 percent APR with daily compounding becomes a 27.1 percent effective rate, turning a $1,000 balance into $1,271.25 after one year.

Mortgages: A $300,000 loan at 4 percent APR yields monthly payments around $1,432 and total interest near $215,520 over thirty years.

Savings accounts: A 6 percent APR with monthly compounding delivers 6.1678 percent APY and grows $1,000 to $1,061.68 in one year.

CDs: A certificate of deposit quoted at 5 percent APY already includes compounding, so you know the exact annual return without conversion.

Converting APR to APY and APY to APR for Accurate Comparisons

To convert APR to APY, use the formula APY = (1 + APR/n)^n − 1. Divide the APR by the number of compounding periods per year, add 1, raise to the power of n, subtract 1. For example, 6.00 percent APR with monthly compounding (n = 12) becomes (1 + 0.06/12)^12 − 1 ≈ 0.061678 or 6.1678 percent APY. If compounding is daily (n = 365), the calculation is (1 + 0.06/365)^365 − 1 ≈ 0.061836 or 6.1836 percent APY. This conversion reveals the true annual rate after all compounding gets applied.

To convert APY back to a nominal APR, use APR = n × ((1 + APY)^(1/n) − 1). Start with the APY, add 1, raise to the power of 1/n, subtract 1, then multiply by n. If you know an account pays 6.1678 percent APY with monthly compounding, the calculation is 12 × ((1.061678)^(1/12) − 1) ≈ 0.06 or 6.00 percent APR. For continuous compounding, the formulas shift to APY = e^(APRcontinuous) − 1 and APRcontinuous = ln(1 + APY), where ln is the natural logarithm. Continuous compounding is rare in consumer products but shows up in some investment models and theoretical finance.

Identify the advertised rate type: Confirm whether the offer lists APR or APY and note the compounding frequency.

Choose the target metric: Decide whether to normalize everything to APY (for yield comparisons) or APR (for nominal rate comparisons).

Apply the conversion formula: Use APY = (1 + APR/n)^n − 1 or the reverse formula depending on direction.

Check continuous compounding: If the product uses continuous compounding, use e^(APR) − 1 to find APY or ln(1 + APY) to find the continuous APR.

Verify the result: Plug a small principal (like $1,000) into both the original and converted rates to confirm the dollar outcomes match after one year.

Side-by-Side Numerical Examples Comparing APR and APY

Three real-world scenarios show how APR and APY diverge in practice. In each case, the nominal APR is the advertised rate, compounding frequency determines the effective APY, and the dollar outcome reveals the true cost or benefit. These examples use round numbers and standard U.S. compounding conventions.

The savings example starts with $1,000 deposited at 6.00 percent APR, compounded monthly. The APY calculation is (1 + 0.06/12)^12 − 1 ≈ 6.1678 percent. After one year, the account balance is $1,000 × 1.061678 ≈ $1,061.68. Simple interest at 6.00 percent would yield only $1,060, so compounding adds $1.68. The credit card example uses a 24.00 percent APR with daily compounding. The effective APY is (1 + 0.24/365)^365 − 1 ≈ 27.1 percent. A $1,000 balance grows to around $1,271.25 after one year, compared to $1,240 under simple interest. The mortgage example finances $300,000 at 4.00 percent APR with monthly payments over thirty years. The monthly rate is 0.04 ÷ 12 ≈ 0.003333, the payment is roughly $1,432, and total interest over 360 months is about $215,520. The advertised APR may run higher if origination fees are included, but the payment calculation uses the nominal periodic rate.

| Scenario | APR | APY | Dollar Outcome |

|---|---|---|---|

| Savings deposit ($1,000, monthly compounding) | 6.00% | 6.1678% | $1,061.68 after one year |

| Credit card ($1,000 balance, daily compounding) | 24.00% | ≈27.1% | $1,271.25 after one year |

| Mortgage ($300,000 loan, 30 years, monthly payments) | 4.00% | n/a (amortized loan) | ~$1,432/month, ~$215,520 total interest |

How to Compare Financial Products Using APR and APY

Start by confirming whether each offer quotes APR or APY. Loan advertisements in the U.S. must disclose APR, which includes interest and certain fees. Deposit accounts typically advertise APY, which already incorporates compounding. If one offer lists APR and another lists APY, you can’t compare the numbers directly without converting both to the same basis.

Check the compounding frequency for every product. Monthly, daily, and continuous compounding all produce different effective yields from the same nominal rate. Convert all rates to APY using the formula (1 + r/n)^n − 1 so you’re comparing apples to apples. Include fees when comparing loans. A lower nominal rate with high origination points can cost more than a slightly higher rate with no fees. Calculate the total dollar cost over your expected holding period. A 0.1 percent APY difference equals $100 per year per $100,000 principal. Over five years on a $200,000 balance, that 0.1 percent gap becomes $1,000.

Identify whether the rate is APR or APY: Read the fine print and confirm the metric used.

Note the compounding frequency: Monthly, daily, quarterly, or continuous compounding changes the effective rate.

Convert both offers to the same basis: Use APY = (1 + APR/n)^n − 1 to standardize comparisons.

Factor in all fees: Add origination charges, annual fees, and closing costs to the interest cost, then annualize over your holding period.

Calculate dollar totals for your term: Plug in your actual principal and time horizon to see the real cost or return in dollars.

Model typical balances for revolving credit: Credit card costs depend on your average daily balance, payment behavior, and grace period usage, not just a single annual snapshot.

Misconceptions and Pitfalls When Comparing APR and APY

One common mistake is comparing an APY savings rate directly to an APR loan rate and assuming the difference is net profit. APY already includes compounding, so a 6 percent APY savings account delivers a 6 percent effective return. A 5 percent APR loan with monthly compounding actually costs you closer to 5.116 percent effective annual rate once you convert it to APY. The nominal 1-percentage-point spread shrinks when you adjust for compounding frequency.

Ignoring fees distorts loan comparisons. A lender advertising 3.75 percent APR might charge two points at closing, raising the true APR to 4.00 percent or higher depending on how long you hold the loan. Another lender quoting 4.00 percent APR with zero points could be cheaper over a short holding period. APR helps standardize these comparisons, but you still need to check the itemized fee schedule and run the math for your expected payoff timeline.

Promotional rates create another trap. A credit card might offer 0 percent APR for twelve months, then revert to 24 percent APR. If you carry a balance into month thirteen, the effective cost over two years is a weighted blend of the promotional and standard rates. A high-yield savings account offering a 5 percent APY intro rate for three months, then dropping to 2 percent APY, delivers far less than 5 percent over a full year. Always compute the weighted average rate across your actual holding period and account for the date when the promotional period ends.

Quick Decision Rules for APR and APY in Everyday Finance

Use APY when comparing any deposit account, savings product, certificate of deposit, or money market fund because APY already includes compounding and shows your true annual return. A higher APY always means more money in your pocket after one year, assuming no fees reduce the balance.

For savings and CDs: Choose the highest APY available, confirming that compounding frequency and fees are already factored into the advertised number.

For loans and mortgages: Compare APR figures that include origination fees, but also calculate the monthly payment and total interest using the nominal periodic rate to understand cash flow.

Always convert rates to the same basis: If one offer quotes APR and another quotes APY, use the conversion formulas to standardize before comparing.

Remember that small percentage differences scale with principal: A 0.1 percent APY edge on $100,000 is $100 per year. On $500,000 it’s $500 per year.

Model your actual behavior: For credit cards, the effective cost depends on whether you pay in full each month (zero interest) or carry a balance (full APR plus compounding applies).

Common Questions About APR and APY Differences

People often ask whether APR is always lower than APY. The answer is no, it depends on context. For savings accounts, APR is the nominal rate and APY is higher because compounding boosts the effective yield. For loans, the advertised APR often includes fees, which can push it above the simple nominal interest rate. If a loan APR includes high upfront costs, it may exceed the effective rate you’d calculate from monthly compounding alone.

Is APR always lower than APY? Not always. APR can include fees that raise it above the nominal rate, and for deposit accounts, APY is typically higher than APR because it reflects compounding.

Which metric should I use to compare loans? Use APR when it includes fees. APR standardizes the total cost across lenders with different fee structures, but always verify what fees are included and calculate total dollar cost for your holding period.

Which metric should I use to compare savings accounts and CDs? Always use APY. It captures the true annual return after compounding, making it the only fair basis for yield comparisons across deposit products.

Final Words

You learned the core difference: APR shows the nominal cost or rate, APY shows the real yearly yield after compounding.

We ran formulas, conversions, and real-dollar examples for savings, credit cards, and mortgages so you can compare like-for-like.

Use simple rules: pick APY for deposit choices, APR (with fees) for loans, and convert when compounding differs.

Understanding how APR and APY differ and why it matters will help you pick the cheaper loan or the better saver. Small choices add up—you’re set to compare with confidence.

FAQ

Q: What is the difference between APR and APY?

A: The difference between APR and APY is APR is the nominal yearly rate (periodic rate × periods) often excluding compounding, while APY is the effective annual yield that includes compounding effects.

Q: When should I use APR versus APY?

A: You should use APR for loans to understand yearly borrowing cost (include fees), and APY for savings or investments to see the real growth after compounding.

Q: Does APR include fees and how does that affect comparisons?

A: APR can include fees to show true borrowing cost, but not always—check disclosures. If fees aren’t included, add them to compare loans fairly by calculating the effective APR.

Q: How do you convert APR to APY and APY to APR?

A: To convert APR to APY use APY = (1 + APR/n)^n − 1; to convert back use APR = n × ((1 + APY)^(1/n) − 1), matching the compounding frequency n.

Q: How does compounding frequency affect APY?

A: Compounding frequency increases APY: more periods (monthly to daily) raise the effective yield slightly. Example: 6% APR → APY 6.1678% monthly, 6.1836% daily.

Q: Is APR always lower than APY?

A: APR isn’t always lower than APY; which is higher depends on compounding and fees. With positive compounding APY exceeds APR, but added fees can shift the comparison.

Q: How do APR and APY affect real dollars — any quick examples?

A: In dollars: $1,000 at 6% APR monthly becomes about $1,061.68 (APY 6.1678%). $1,000 on 24% APR credit card with daily compounding grows to about $1,271.25 (APY ≈27.1%).

Q: How should I compare financial products using APR and APY?

A: To compare products, identify which rate is quoted, check compounding frequency, convert rates to the same basis, include fees, then model the dollar outcome for your holding period.

Q: What common mistakes should I avoid when comparing APR and APY?

A: Common mistakes include comparing APR to APY directly, ignoring compounding frequency, overlooking fees or short promotional rates, and using the wrong holding period for your calculation.

Q: What quick decision rules help pick between APR and APY?

A: Quick rules: use APY for savings comparisons, use APR (with fees) for loans, convert both to the same compounding basis, and remember small percent gaps matter on big balances.

{kind=link}